In challenging economic times it’s important that employers can demonstrate the valuable benefits they offer to staff, such as a good quality pension scheme. The latest Nest webinar aimed to help employers do just that.

With presenters from across Nest, the webinar covered the trends we’re seeing amongst Nest savers during the cost-of-living crisis and how we’re positioning our investment portfolios to aim to deliver growth over the longer term. It also give viewers some actionable tips to help their workers keep their records up to date by telling us who they’d like to inherit their pot.

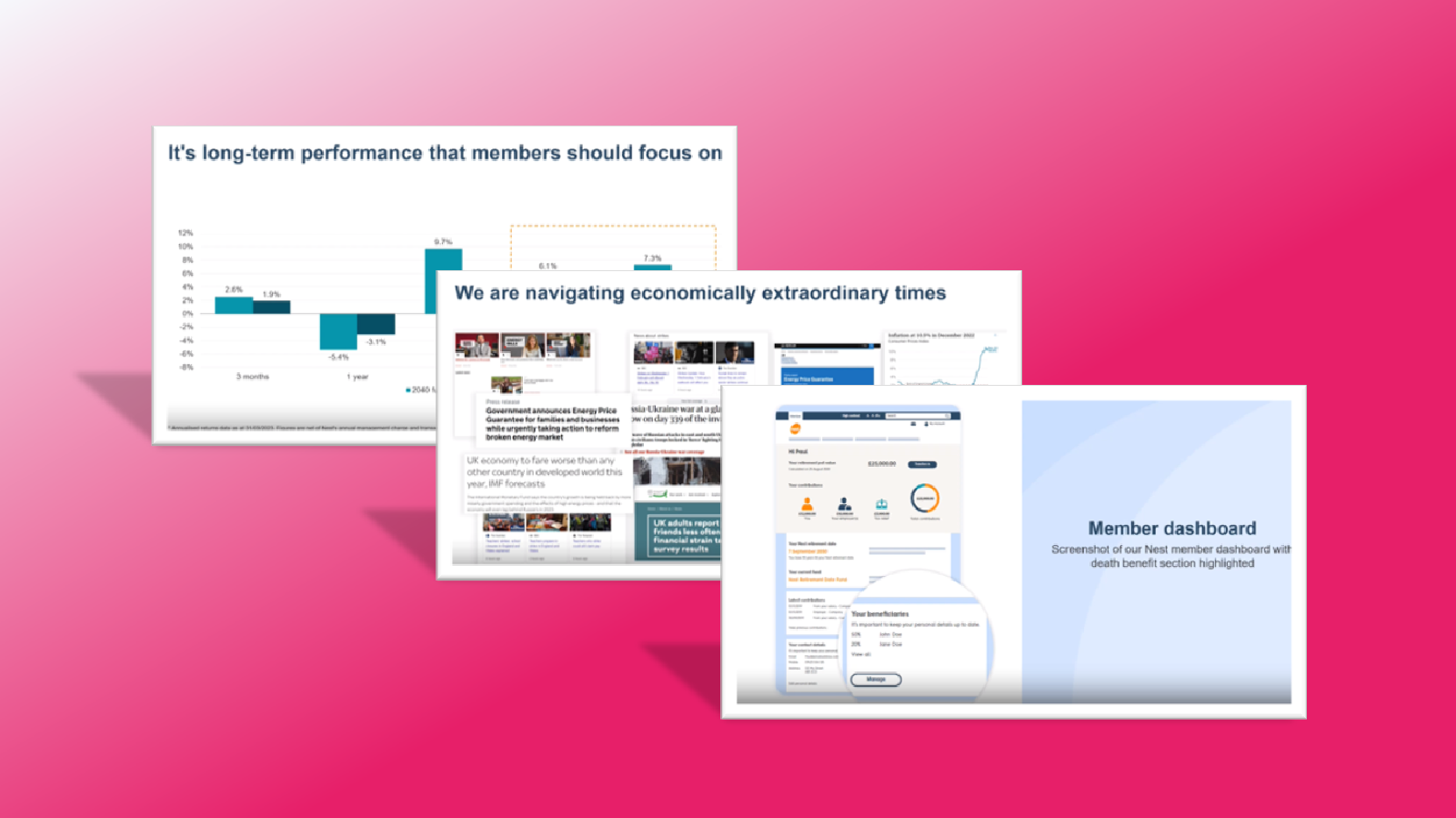

All the presentations are available below to watch again or share with colleagues:

Investment update 2023 – Mark Fawcett, Chief Investment Officer, Nest

The Cost-of-Living Crisis – The view from Nest members and employers – Ric Tizard, Head of Customer Insight, Nest

Important actions for your workers to take – David Knight, Head of Strategic Account Management, Nest

The slides from the webinar are available here: April employer webinar 23.

During the webinar we received a number of questions, answers to them can be found below.

- How do employers tell people how to sign up for their online access?

We have lots of collateral in the online employee engagement toolkit, this is covered in the section headed

“New Starters”. https://www.nestpensions.org.uk/schemeweb/nest/employers/managing-scheme/communication/starters.html

- How do employees at retirement age tell you that they are not retiring so their funds can be invested more appropriately?

All our default funds are target dated, set to your state pension retirement age. As an example, if a member is in the 2023 target dated fund but they don’t intend on retiring until 2030 they can follow the steps below to keep us updated. There is no charge to do this and can be done in a few clicks:

- Login online, navigate to ‘my account’ in the top left of the page

- Select ‘edit profile’

- At the bottom of this page you can change your retirement date.

- As the employer administering the pension scheme can I see which members have logged in to their online account?

We can see who has logged in, but we are not able to share this information on an employer-by-employer basis. If you are going to promote account registration for Nest we would suggest that you do this with all of your Nest members.

- Does Nest have a service to help track down previous pensions from previous employers?

No, there is already a tracing service available to workers (the pension tracing service) which has been running for a number of years and the introduction by the government of the pensions dashboard should make this even easier. Nest supports the pension dashboard.

- Can Nest pension members increase their contributions though their login?

Yes, and they can do this online and by direct debit if they want to make regular payments. However, our research shows that employers who allow increased pension contributions through payroll see more members making additional contributions.

- Has Nest considered creating an app for members?

We don’t currently offer an app for members; however, all of our webpages and user journeys have been optimised for use on mobiles. We monitor all our journeys closely to understand how members interact with them. This includes looking at the logging in journey to understand what’s working well, if there are any pain points, and the devices that our members use. If members are struggling to login, support is available through our online Help Centre or Contact Centre.

- Can you clarify the difference between expression of wish and nominated beneficiaries on Nest? Is the nominated beneficiary subject of IHT?

A nomination is a legally binding instruction which we must follow, and the amount will be included in the member’s estate. The expression of wish is as the name suggests the member is saying what they would like to happen. It is not legally binding on Nest and our trustees can make changes to this if appropriate. Normally the benefit when paid following an expression of wish does not form part of the member’s estate. Death benefits included in the member’s estate may be subject to inheritance tax but this depends on the size of the member’s estate, very few estates in the UK pay this tax.

- On death is the Pension Fund paid in total i.e. the balance of the fund to whoever is named as beneficiary or is it paid as per the pension plan payments chosen…monthly or yearly?

We pay out the full value of the fund and this is normally a lump sum payment.

- If a member nominates rather than expresses a wish, as this is legally binding is it, or could it, be subject to inheritance tax?

A nomination is legally binding, and it will form part of the member’s estate. If the member’s estate is big enough, inheritance tax will be payable and so this could mean inheritance tax is paid on this payment.

- Would the value of the fund being paid out be paid out as a lump or weekly/monthly as a usual pension payment

The death benefit is normally paid as a lump sum. If the member survives to retirement and wants to draw their pension this can be paid as a lump sum, or a regular payment or a mix of both.